Interactive online version:

HA-SSJs in Life-Cycle Models#

[1]:

# Basic imports

from HARK.models import IndShockConsumerType

from HARK.utilities import plot_SSJ

from HARK.ConsumptionSaving.ConsIndShockModel import init_lifecycle

from time import time

mystr = lambda x: "{:.3f}".format(x)

The “sequence space Jacobian” approach, first described by Auclert et al (2021), has rapidly become quite popular in heterogeneous agents macroeconomics. While the original paper only laid out how to construct HA-SSJ matrices (with the “fake news” algorithm) for standard infinite horizon or perpetual youth models, one of its authors has very recently teamed up with Econ-ARK contributor Mateo Velasquez-Giraldo to extend the algorithm to life-cycle models.

This new HA-SSJ capability for life-cycle models has been incorporated into HARK, using the same make_basic_SSJ interface as for standard infinite horizon models. If you haven’t already, we recommend that you read our basic SSJ tutorial notebook before going further here.

Key Restriction: “Flat” Population Dynamics#

As forewarning, not all life-cycle models are currently compatible with HARK’s automatic HA-SSJ computation. The key restriction is that the model’s population dynamics must be “flat” or invariant to the shock of interest. This means two things.

First, the model itself cannot have agent survival be endogenous to agent behavior, as in a model with endogenous health through medical care or other choices. For almost any interesting shock, those agent behaviors will be affected, and thus population dynamics will be affected by the shock.

Second, even if survival is exogenous within the microeconomic model, it also cannot be perturbed by the shocked variable. For example, MarkovConsumerType can be used to specify a model with persistent unemployment in which unemployed agents are less likely to survive to the next period. This model could be used if you were interested in shocks to the interest rate Rfree and/or the wage rate WageRte. However, if the shock variable involves the transition probabilities between

employment states, then survival probabilities will be indirectly affected, and thus population dynamics are not “flat”.

We are working on generalizing the method so we can lift this restriction.

Additional Options for Life-Cycle Models#

The basic syntax for using make_basic_SSJ is the same for a life-cycle model as for a standard infinite horizon model. If you have an instance of an AgentType subclass named Agent, then you can do:

SSJs = Agent.make_basic_SSJ(shock, outcomes, grids)

The shock names a single age-varying model parameters that (directly or indirectly) affects the life-cycle problem (the \(x\)), and the outcomes are the names of one or more more model variables whose effects we are interested in (the \(Y\)s).

Just like with an infinite horizon model, you can optionally name a Harmenberg norm to more efficiently handle permanent income normalization (and thus skip providing a grid for pLvl). For most permanent-income-normalized models in HARK, this is PermShk.

NB: Please see the basic tutorial notebook for additional options that are also available for life-cycle models.

Whether or not you use the “Harmenberg trick” in a permanent-income-normalized model, you must name the normalization trend if one exists. In most normalized HARK models, permanent income growth has an expected value in each period given by PermGroFac, so you would pass trend="PermGroFac" to make_basic_SSJ. Failing to do this will result in the HA-SSJ output being incorrectly weighted by age and thus wrong.

If there is ongoing population growth, so that each successive cohort is \(P\) times the size of the prior one, then the value of \(P\) should be passed as the pop_gro argument to the method. NB: This functionality is not yet implemented.

If there is ongoing productivity growth, so that the level of each successive cohort’s variables (at model entry) grows by factor \(G\) relative to the prior cohort, then the value of \(G\) should be passed as the prod_gro argument to the method. NB: This functionality is not yet implemented.

If you wish to examine the age-specific HA-SSJ matrices (i.e. you do not want the output to be summed across ages), then you should pass age_agg=False to the method.

Example Life-Cycle HA-SSJ#

As in the basic tutorial, we will use HARK’s workhorse IndShockConsumerType as our example model, but with an off-the-shelf life-cycle dictionary. The details don’t really matter, but the dictionary init_lifecycle represents high-school-educated men who enter the model at age 25, live to age 90 at most, and have an income process as estimated by Cagetti (2003) for growth factors and Sabelhaus and Song (2010) for income risk.

[2]:

# Make a life-cycle agent using an off-the-shelf dictionary

MyType = IndShockConsumerType(**init_lifecycle)

As usual, we need to specify grids for state variables. Continuous variables need at least a min and a max, as well as a number of gridpoints N. By default, linear spacing is used, but you can set a polynomial order or a level of exponential nesting as nest. Alternatively, you can specify a custom grid in the custom key. For a discrete state, only the number of values N needs to be given.

You must provide a grid for all arrival variables (other than the one that is normalized out, if you use norm), as well as for any outcome variables that are requested. The exception is for an outcome that twists to an arrival variable. E.g., aNrm[t] --> kNrm[t+1] in many HARK models, so you do not need to provide a grid for aNrm once the grid for (arrival variable) kNrm has been provided.

[3]:

# Define grid specifications

wealth_grid = {"min": 0.0, "max": 40.0, "N": 250, "order": 2.0}

con_grid = {"min": 0.0, "max": 10.0, "N": 201}

my_grid_specs = {"kNrm": wealth_grid, "cNrm": con_grid}

That’s all of the setup we need to do! Let’s construct the HA-SSJs with respect to the interest factor Rfree.

Because HARK’s solver for IndShockConsumerType treats Rfree[t] as representing next period’s interest rate (when computing expectations over future states), we need to designate the shock as offset=True so that the timing is parsed correctly.

We will use the “Harmenberg trick” with PermShk as the shock to be renormalized in the probability measure, so norm="PermShk" is also passed.

Finally, permanent income grows by factor PermGroFac each period, so we specify that trend="PermGroFac" to ensure proper weighting by age.

About 9-10 times more periods need to be solved and then converted to grid/matrix format for a life-cycle model as compared to an infinite horizon HA-SSJ construction, so this method will take about 50 seconds to run.

[4]:

# Make HA-SSJs for the life-cycle model

t0 = time()

J_A_R, J_C_R = MyType.make_basic_SSJ(

"Rfree", # name of the parameter to be shocked

["aNrm", "cNrm"], # name(s) of the outcome variable(s) we're interested in

my_grid_specs, # dictionary of grid specifications

offset=True,

norm="PermShk",

trend="PermGroFac",

)

t1 = time()

print(

"Constructing those HA-SSJs for a life-cycle model took "

+ mystr(t1 - t0)

+ " seconds."

)

Constructing those HA-SSJs for a life-cycle model took 49.470 seconds.

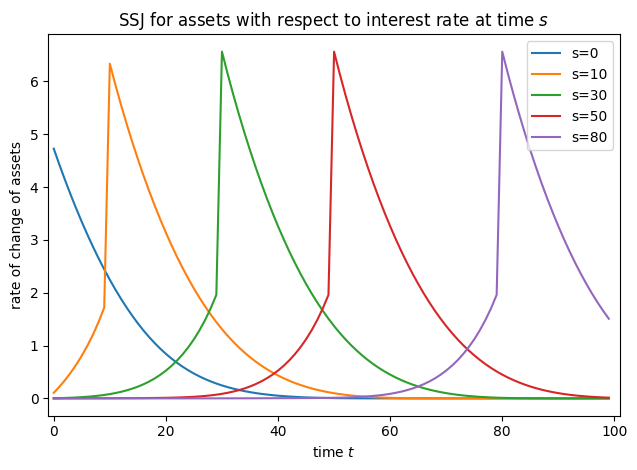

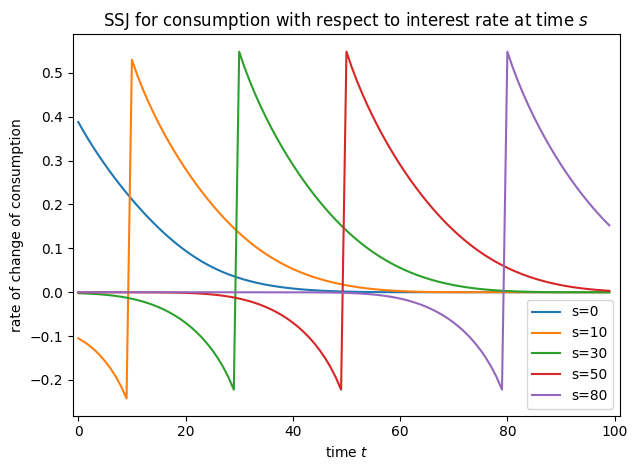

We can now plot the SSJs for assets and consumption with respect to the interest rate. They look an awful lot like the ones from the infinite horizon example, and that’s no coincidence!

[5]:

# Plot select columns of the HA-SSJs

plot_SSJ(J_A_R, [0, 10, 30, 50, 80], "assets", "interest rate")

plot_SSJ(J_C_R, [0, 10, 30, 50, 80], "consumption", "interest rate")

The outcomes are calculated as population averages, and thus the rate of change of the outcomes should also be interpreted this way. This is the major reason why the life-cycle algorithm is restricted to “flat” population dynamics, so that the level of the outcomes can be specified analogously to the infinite horizon model. In the presence of endogenous population dynamics (through agent behavior or through shocks), regularizing by population size must be handled a bit differently. This is an area of near future development in HARK.