Overview#

Introduction to HARK

Learning About HARK

A Gentle Introduction to HARK

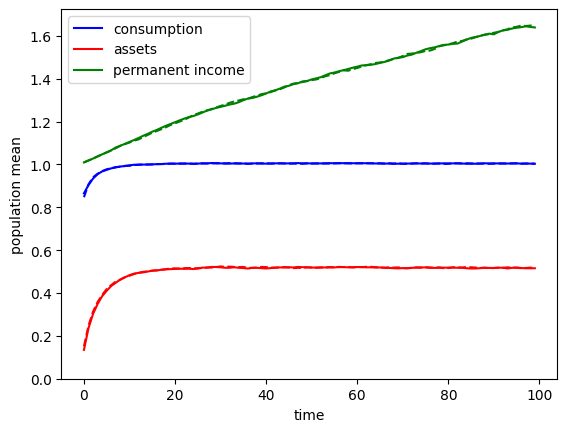

Simulating Microeconomic Models

The Nature of Time for AgentTypes

Constructed Attributes and Model Defaults

Advanced and Uncommon HARK Concepts

Numeric Methods Commonly Used in HARK

Directory of Consumption-Saving Models

Elements of an AgentType Subclass

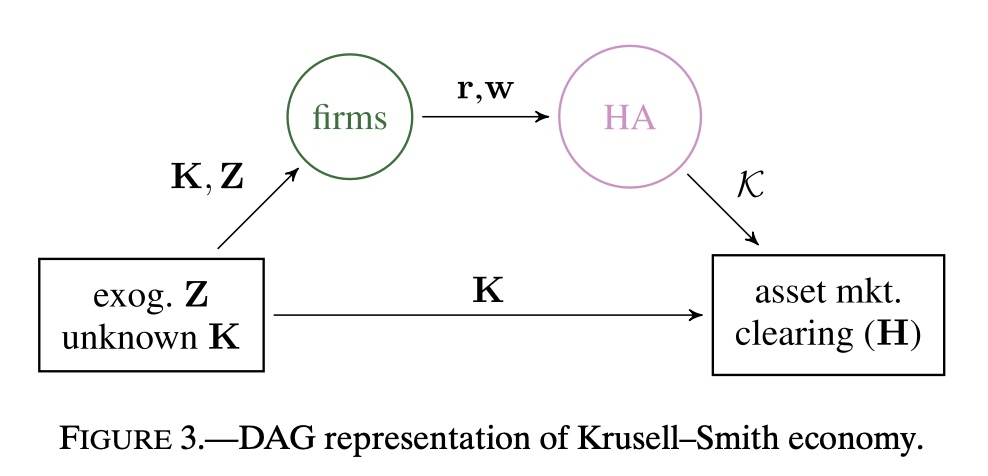

“Macroeconomic” Models: the Market Class

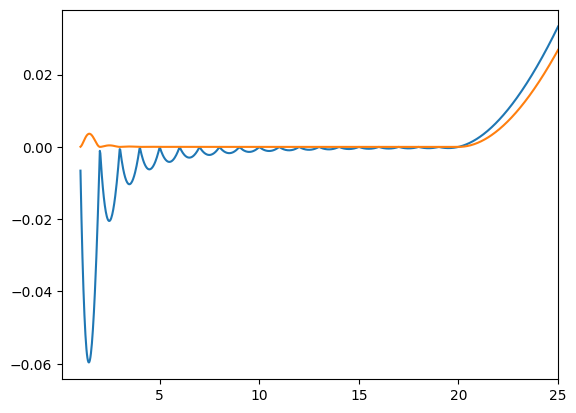

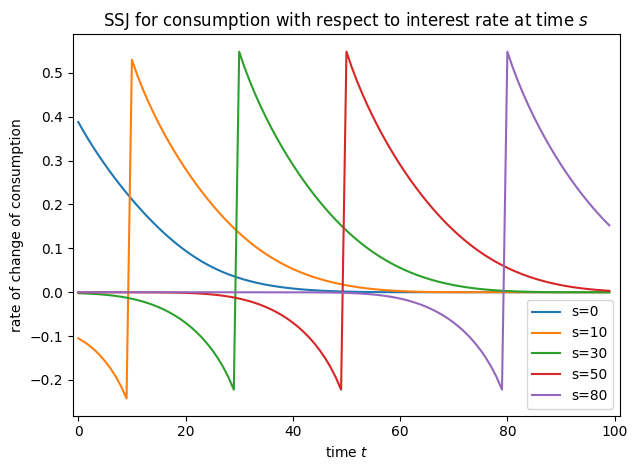

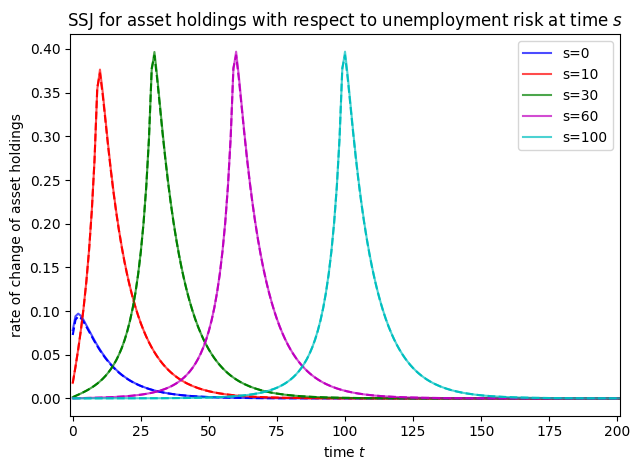

The Sequence Space Jacobian (SSJ) method

Making HA-SSJ Matrices with HARK

Advanced Examples of HA-SSJ’s

HA-SSJs in Life-Cycle Models

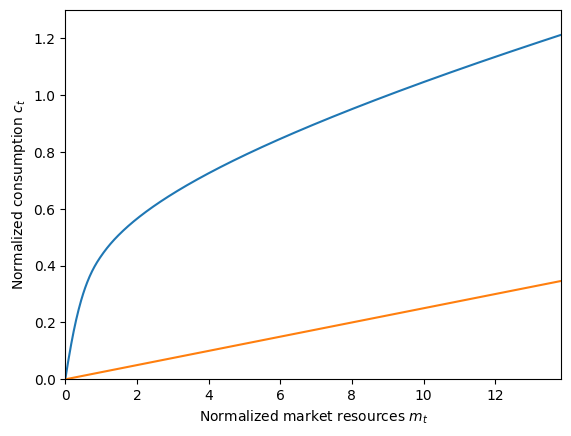

Consumption-Saving Models

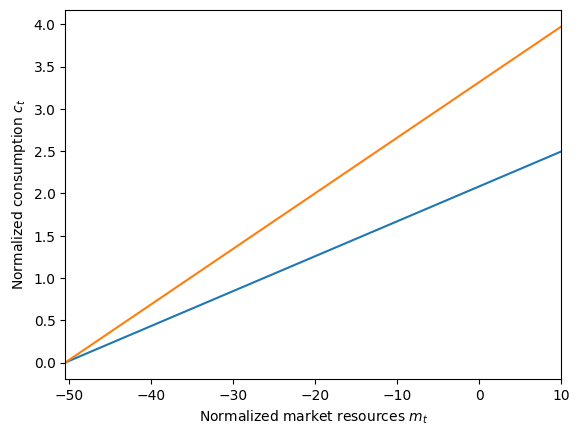

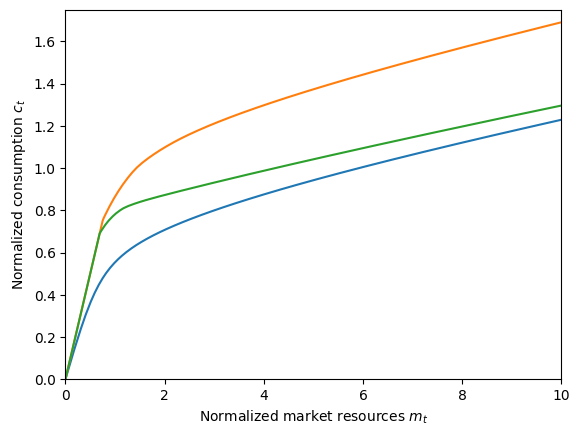

Perfect Foresight Model

Tractable Buffer Stock Model

Representative Agent Models

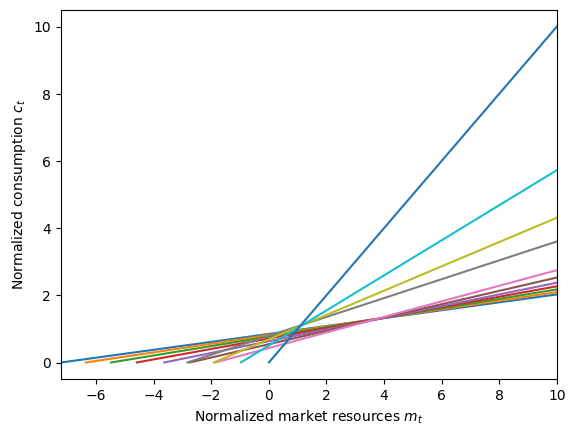

Permanent and Transitory Income Shocks

Higher Interest Rate to Borrow than Save

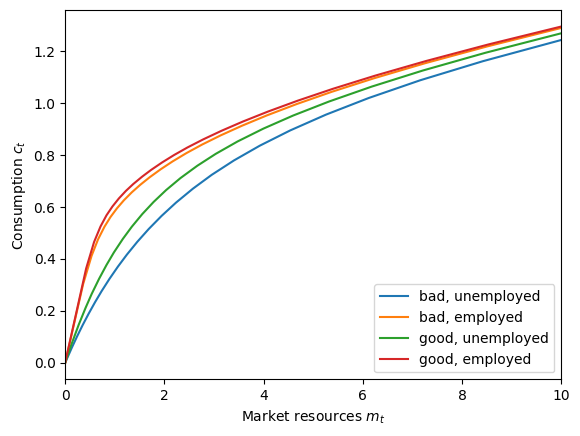

Discrete State with Markov Transitions

Generalized Income Process

Aggregate Productivity Shocks

Aggregate Productivity Shocks with a Discrete State

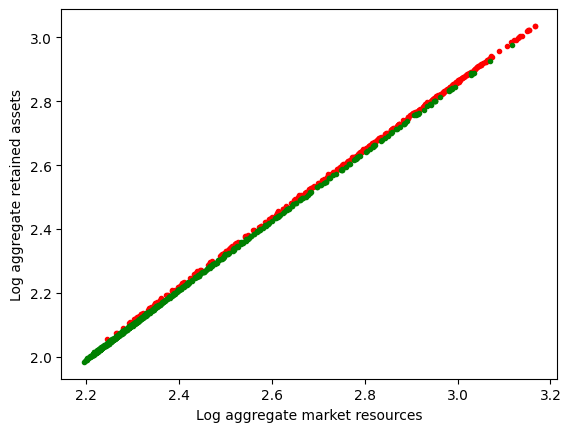

Krusell-Smith Model

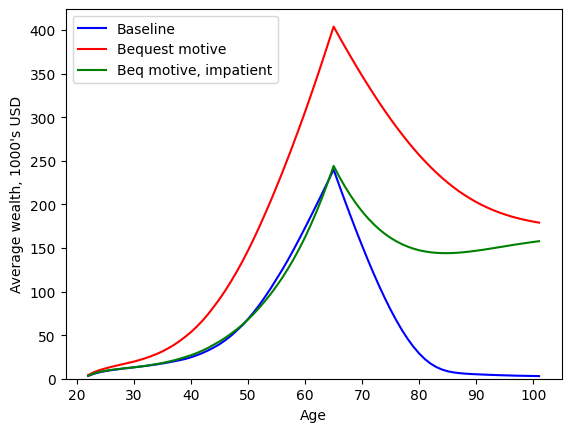

Warm Glow Bequest Motives

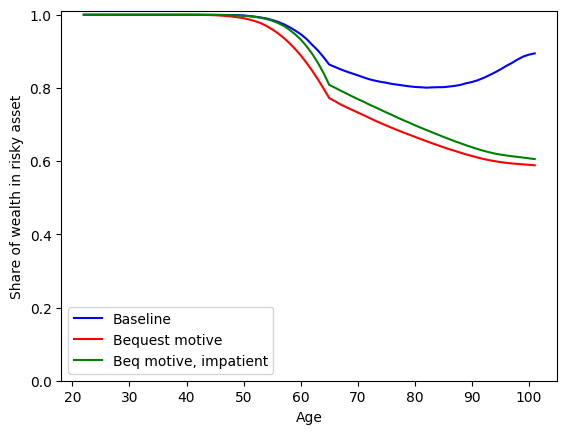

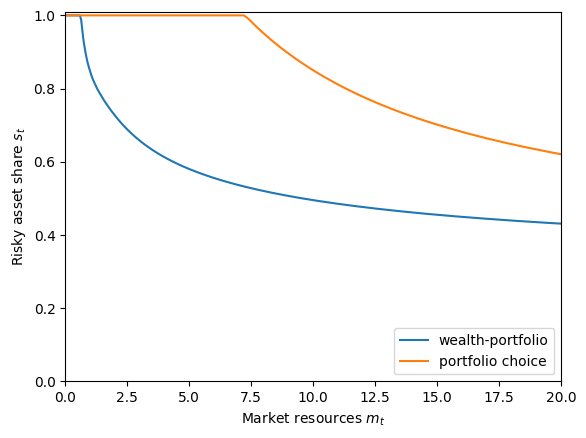

Warm-Glow Bequest Motive and Portfolio Choice

Wealth-in-Utility Multiplicatively with Consumption

Wealth-in-Utility Additively with Consumption

Habit Formation

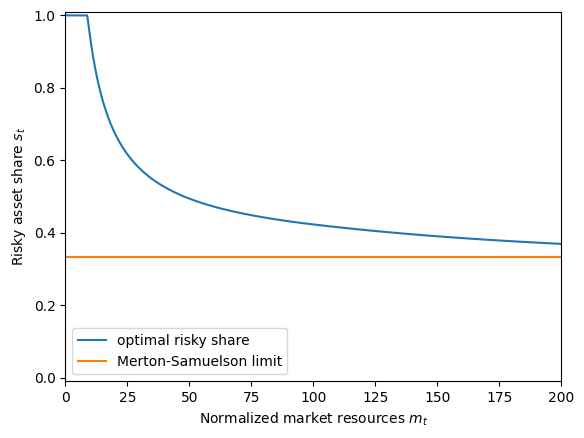

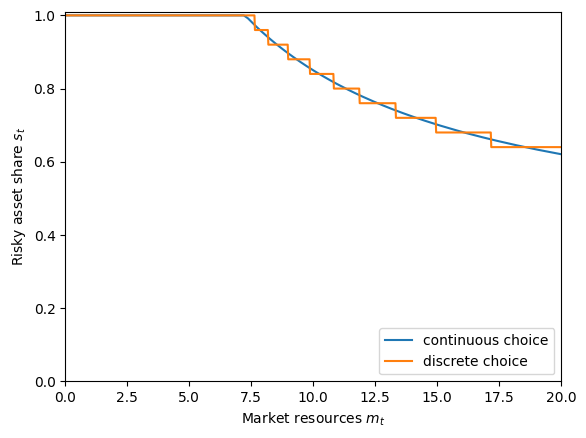

Assets with Risky Returns: Portfolio Choice

Advanced Options for Portfolio Allocation Models

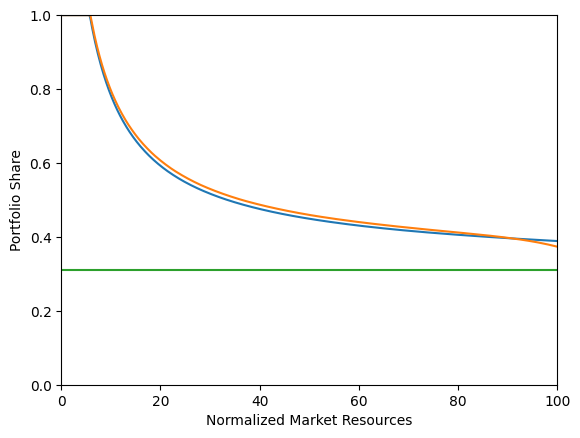

Multiplicative Wealth-in-Utility with Portfolio Choice

Portfolio Allocation with “Sequential Solvers”

Habit Formation with Portfolio Choice

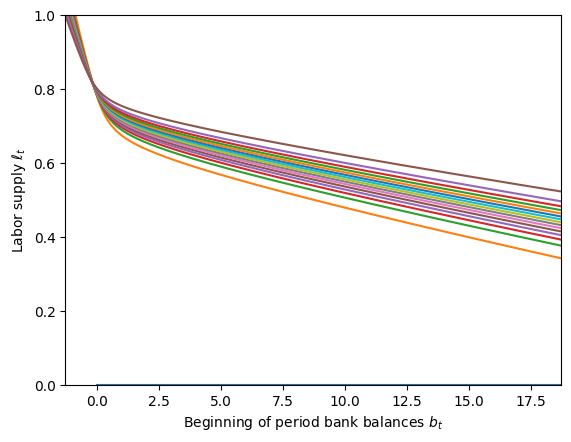

Intensive Margin Labor Supply Choice

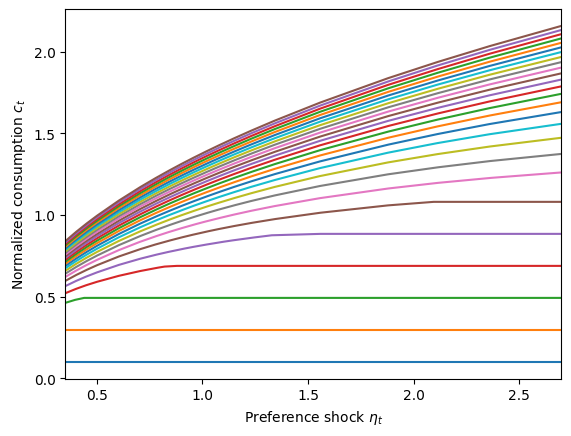

Preference Shocks to Consumption Utility

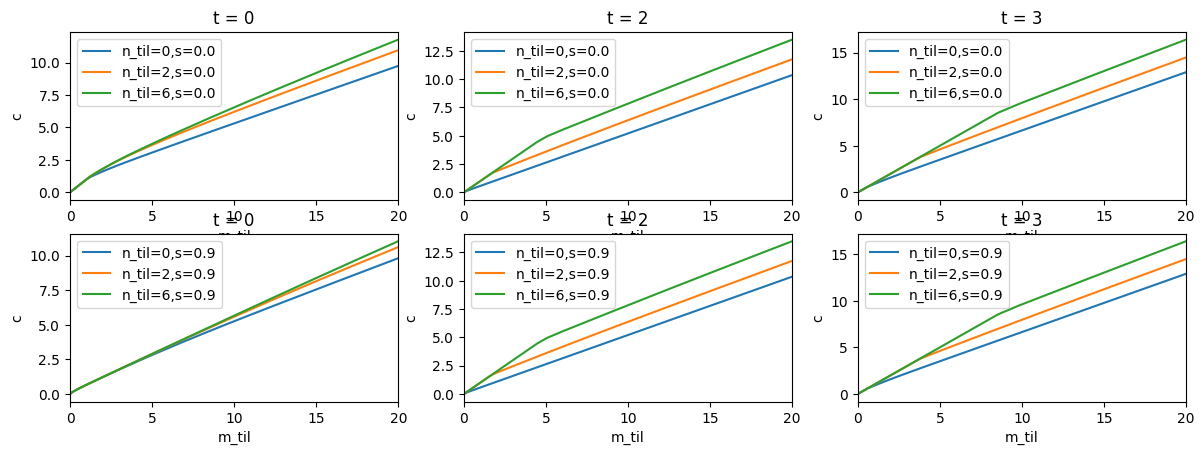

Basic Health Investment

Medical Care on the Intensive Margin

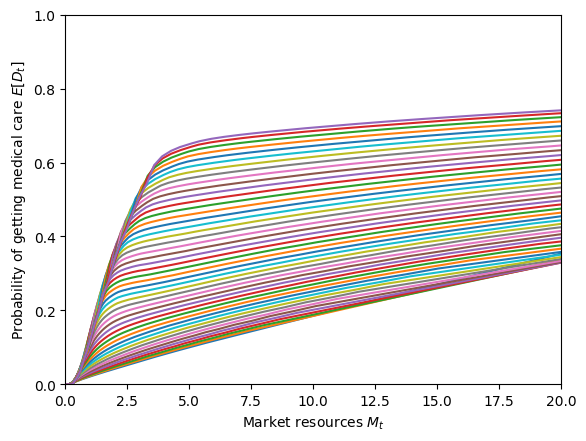

Medical Care on the Extensive Margin

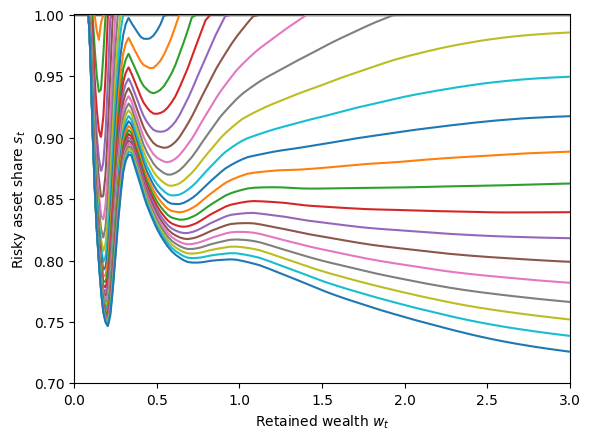

“Risky Contribution” Model

Examples

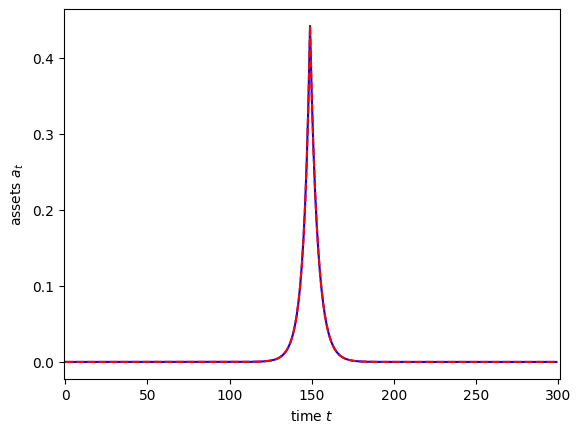

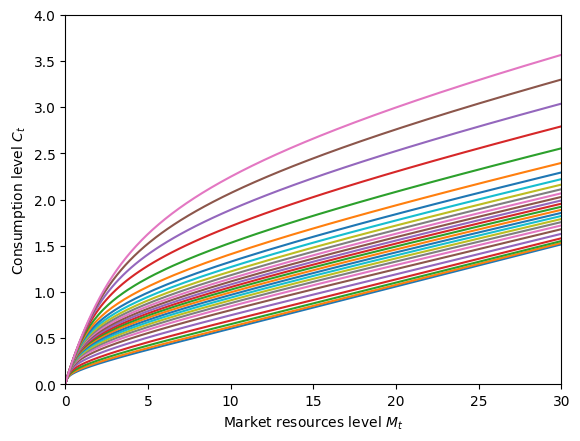

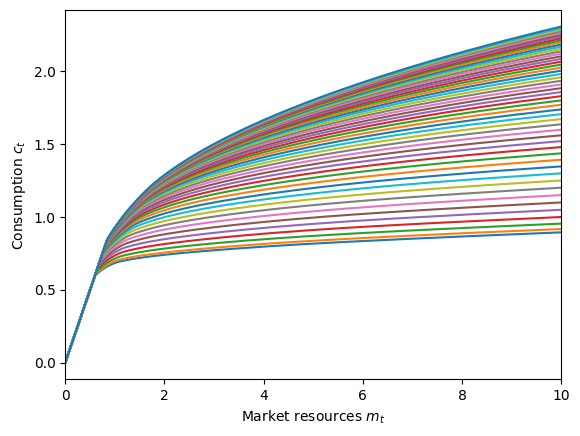

A Life Cycle Model: The Distribution of Assets By Age

Transition Matrix vs Monte Carlo Methods for Heterogeneous-Agent Models

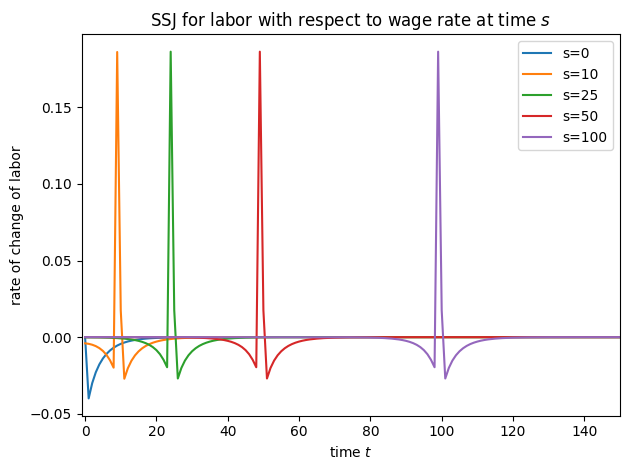

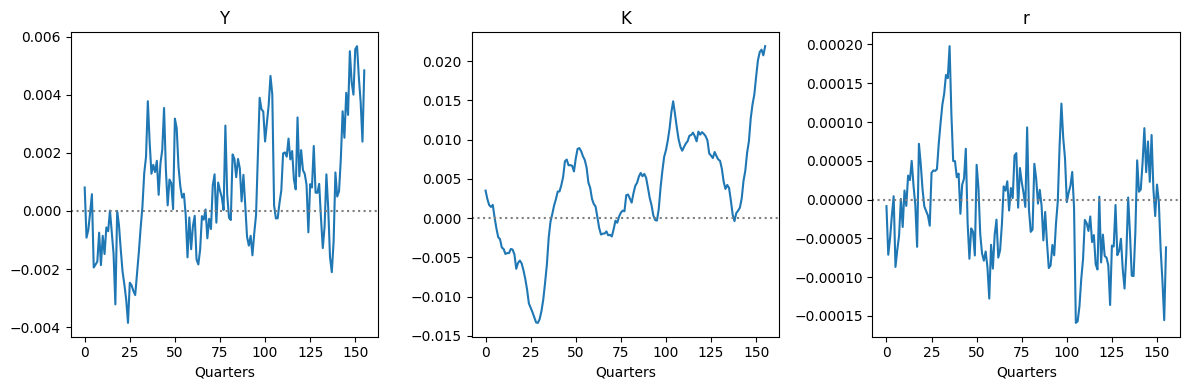

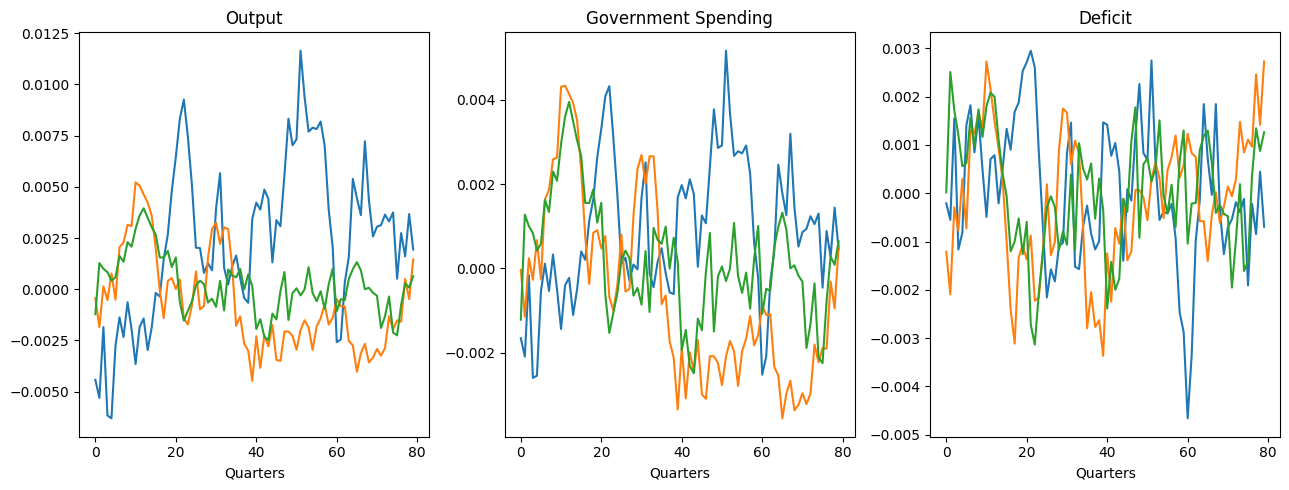

Computing Heterogenous Agent Sequence Space Jacobians in HARK

Solving Krusell Smith Model with HARK and SSJ

HARK and the Sequence Space Jacobian (SSJ) Method

Journey: Economics PhD Student