Interactive online version:

Discrete State with Markov Transitions#

This module defines consumption-saving models in which an agent has CRRA utility over consumption, geometrically discounts future utility flows and expects to experience transitory and permanent shocks to his/her income. Moreover, in any given period s/he is in exactly one of several discrete states. This state evolves from period to period according to a Markov process.

[1]:

from time import time

import numpy as np

import matplotlib.pyplot as plt

from HARK.ConsumptionSaving.ConsMarkovModel import (

MarkovConsumerType,

make_ratchet_markov,

)

from HARK.distributions import DiscreteDistributionLabeled

from HARK.utilities import plot_funcs

mystr = lambda number: f"{number:.4f}"

Model Statement#

In this model, an agent is very similar to the one in the “idiosyncratic shocks” model of ConsIndShockModel , except that here, an agent’s income distribution (\(F_{t+1}\)), permanent income growth rate \(\Gamma_{t+1}\), survival probability \(\mathsf{S}_t\), and interest factor \(R\) are all functions of the Markov state and might vary across states.

\(\newcommand{\CRRA}{\rho}\) \(\newcommand{\LivPrb}{\mathsf{S}}\) \(\newcommand{\PermGroFac}{\Gamma}\) \(\newcommand{\Rfree}{\mathsf{R}}\) \(\newcommand{\DiscFac}{\beta}\)

The agent’s problem can be written in Bellman form as:

\begin{eqnarray*} \text{v}_t(m_t,s_t) &=& \max_{c_t} u(c_t) + \beta \mathsf{S}_{t}(s_t) \mathbb{E} [\text{v}_{t+1}(m_{t+1}, s_{t+1}) ], \\ a_t &=& m_t - c_t, \\ a_t &\geq& \underline{a}, \\ m_{t+1} &=& \frac{R(s_{t+1})}{\Gamma(s_{t+1})\psi_{t+1}} a_t + \theta_{t+1}, \\ (\psi_{t+1},\theta_{t+1}) &\sim& F_{t+1}(s_{t+1}), ~~~ \mathbb{E} [\psi_t ~|~ s_t] = 1, \\ Prob[s_{t+1}=j| s_t=i] &=& \triangle_{t,ij}, \\ u(c) &=& \frac{c^{1-\rho}}{1-\rho}. \end{eqnarray*}

The Markov matrix \(\triangle_t\) specifies transition probabilities from current state \(i\) to future state \(j\).

The class MarkovConsumerType extends IndShockConsumerType to represents agents in this model.

Example Parameters for a MarkovConsumerType#

The parameters to specify a MarkovConsumerType are mostly the same as for the familiar IndShockConsumerType , but with some key differences and additions. Most notably, model parameters that are discrete-state-varying must be specified as a list of values, or a nested list if the parameter is both time-varying and discrete-state-varying. Because the income distribution \(F_t\) depends on both age and the discrete state, parameters that describe the income process are nested lists

(when using the default constructor).

Second, the Markov transition matrix \(\Delta_t\) must be specified in some way. In the default dictionary, the Markov process is binary, and specified with (age-dependent) probabilities of remaining in each state, Mrkv_p11 and Mrkv_p22. This behavior can be changed by setting the MrkvArray entry in the constructors dictionary; HARK provides a couple other example constructors. If your MrkvArray will not be produced by a parametric constructor function (e.g., maybe it’s

result of some other model output), just set constructors["MrkvArray"] = None in your parameter dictionary to turn off the constructor apparatus.

Param |

Description |

Code |

Value |

Constructed |

|---|---|---|---|---|

\(\DiscFac\) |

Intertemporal discount factor |

|

\(0.96\) |

|

\(\CRRA\) |

Coefficient of relative risk aversion |

|

\(2.0\) |

|

\(\Rfree_t\) |

Risk free interest factor |

|

\([[1.03, 1.03]]\) |

\(\surd\) |

\(\LivPrb_t\) |

Survival probability |

|

\([[0.98,0.98]]\) |

\(\surd\) |

\(\PermGroFac_{t}\) |

Permanent income growth factor |

|

\([[0.99, 1.03]]\) |

\(\surd\) |

\(\sigma_\psi\) |

Standard deviation of log permanent income shocks |

|

\([[0.1,0.1]]\) |

\(\surd\) |

\(N_\psi\) |

Number of discrete permanent income shocks |

|

\(7\) |

|

\(\sigma_\theta\) |

Standard deviation of log transitory income shocks |

|

\([[0.1,0.1]]\) |

\(\surd\) |

\(N_\theta\) |

Number of discrete transitory income shocks |

|

\(7\) |

|

\(\mho\) |

Probability of being unemployed and getting \(\theta=\underline{\theta}\) |

|

\([0.05,0.05]\) |

|

\(\underline{\theta}\) |

Transitory shock when unemployed |

|

\([0.3,0.3]\) |

|

\(\mho^{Ret}\) |

Probability of being “unemployed” when retired |

|

\(0\) |

|

\(\underline{\theta}^{Ret}\) |

Transitory shock when “unemployed” and retired |

|

\(0.0\) |

|

\((none)\) |

Period of the lifecycle model when retirement begins |

|

\(0\) |

|

\((none)\) |

Minimum value in assets-above-minimum grid |

|

\(0.001\) |

|

\((none)\) |

Maximum value in assets-above-minimum grid |

|

\(20.0\) |

|

\((none)\) |

Number of points in base assets-above-minimum grid |

|

\(48\) |

|

\((none)\) |

Exponential nesting factor for base assets-above-minimum grid |

|

\(3\) |

|

\((none)\) |

Additional values to add to assets-above-minimum grid |

|

\(None\) |

|

\(\underline{a}\) |

Artificial borrowing constraint (normalized) |

|

\(0.0\) |

|

\((none)\) |

Indicator for whether |

|

\(True\) |

|

\((none)\) |

Indicator for whether |

|

\(False\) |

|

\(s_0\) |

Distribution of discrete state at model entry |

|

\([1.0, 0.0]\) |

|

\(\Delta_{t,00}\) |

Probability of remaining in the first discrete state |

|

\([0.9]\) |

\(\surd\) |

\(\Delta_{t,11}\) |

Probability of remaining in the second discrete state |

|

\([0.4]\) |

\(\surd\) |

The constructor function make_simple_binary_markov uses the parameters Mrkv_p11 and Mrkv_p22 (as well as T_cycle ) to build MrkvArray , a list with a single \(2 \times 2\) array in it.

Example Implementations of MarkovConsumerType#

When the solve method of a MarkovConsumerType is invoked, the solution attribute is populated with a list of ConsumerSolution objects, which each have the same attributes as the “idiosyncratic shocks” model. However, each attribute is now a list (or array) whose elements are state-conditional values of that object.

For example, in a model with 4 discrete states, each the cFunc attribute of each element of solution is a length-4 list whose elements are state-conditional consumption functions. That is, cFunc[2] is the consumption function when \(s_t = 2\).

ConsMarkovModel is compatible with cubic spline interpolation for the consumption functions, soCubicBool = True will not generate an exception. The problem is solved using the method of endogenous gridpoints, which is moderately more complicated than in the basic ConsIndShockModel.

Several variant examples of the model will be illustrated below:

Default parameters with binary growth states

Model with serially correlated unemployment

Model with period of “unemployment immunity”

Model with serially correlated permanent income growth

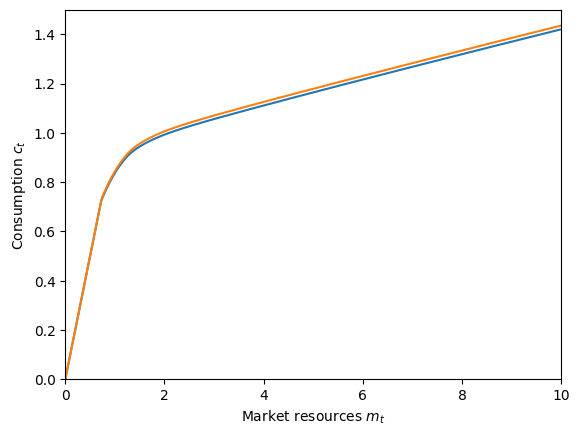

Default parameters: binary growth states#

When MarkovConsumerType is used “off the shelf”, the default parameters generate a binary Markov process in which the two states differ only in the expected growth rate of permanent income \(\PermGroFac_t\); the first (index 0 ) state has lower expected growth and the second state (index 1 ) has higher expected growth.

Let’s make and solve an infinite horizon model with the default parameters, then plot the consumption function for each state.

[2]:

# Make and solve a default MarkovConsumerType

DefaultType = MarkovConsumerType(cycles=0)

t0 = time()

DefaultType.solve()

DefaultType.unpack("cFunc")

t1 = time()

print("Solving the model with default parameters took " + mystr(t1 - t0) + " seconds.")

Solving the model with default parameters took 0.4751 seconds.

[3]:

# Plot the consumption functions

plt.ylim(0.0, 1.5)

plot_funcs(

DefaultType.cFunc[0],

0.0,

10.0,

xlabel=r"Market resources $m_t$",

ylabel=r"Consumption $c_t$",

)

Well that’s not very interesting. Let’s try something else.

Serially correlated unemployment#

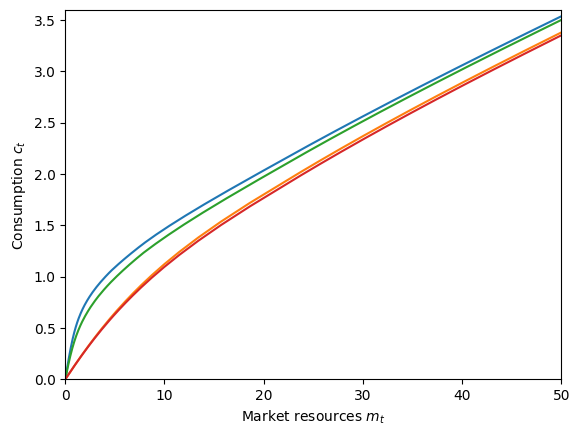

Let’s specify a model for consumers who face serially correlated unemployment during boom or bust cycles of the economy. We’ll specify income as binary within each state: you get something or you get nothing. There will be four discrete Markov states, indexed in this order: employed-boom, unemployed-boom, employed-bust, unemployed-bust.

First, let’s define a function that constructs the Markov transition matrix for this model.

[4]:

# Define the Markov transition matrix for serially correlated unemployment

def make_serial_unemployment_boombust_mrkv(

UnempDur, BoomDur, BustDur, UrateG, UrateB, T_cycle

):

"""

Construct a (constant over time) Markov transition matrix representing serially

correlated unemployment with boom and bust cycles.

Parameters

----------

UnempDur : float

Average duration of an unemployment spell, in both states.

BoomDur : float

Average duration of a boom.

BustDur : float

Average duration of a bust.

UrateG : float

Unemployment rate in boom times, if they went on indefinitely.

UrateB : float

Unemployment rate in bust times, if they went on indefinitely.

T_cycle : float

Number of periods in the cycle; only used to replicate the Markov matrix.

Returns

-------

MrkvArray : [np.array]

List with T copies of a 4x4 Markov transition array.

"""

p_reemploy = 1.0 / UnempDur

p_unemploy_good = p_reemploy * UrateG / (1 - UrateG)

p_unemploy_bad = p_reemploy * UrateB / (1 - UrateB)

boom_prob = 1.0 / BustDur

bust_prob = 1.0 / BoomDur

MrkvArray_t = np.array(

[

[

(1 - p_unemploy_good) * (1 - bust_prob),

p_unemploy_good * (1 - bust_prob),

(1 - p_unemploy_good) * bust_prob,

p_unemploy_good * bust_prob,

],

[

p_reemploy * (1 - bust_prob),

(1 - p_reemploy) * (1 - bust_prob),

p_reemploy * bust_prob,

(1 - p_reemploy) * bust_prob,

],

[

(1 - p_unemploy_bad) * boom_prob,

p_unemploy_bad * boom_prob,

(1 - p_unemploy_bad) * (1 - boom_prob),

p_unemploy_bad * (1 - boom_prob),

],

[

p_reemploy * boom_prob,

(1 - p_reemploy) * boom_prob,

p_reemploy * (1 - boom_prob),

(1 - p_reemploy) * (1 - boom_prob),

],

],

)

MrkvArray = T_cycle * [MrkvArray_t]

return MrkvArray

Now we create a dictionary that specifies the parameters for our consumers, and put our custom-defined Markov array constructor into the constructors dictionary within the parameter dictionary. Because we will be using a very simple custom income distribution, we override the default constructors for IncShkDstn (with lognormal shocks and unemployment) by setting them to None .

[5]:

# Make a consumer with serially correlated unemployment, subject to boom and bust cycles

init_serial_unemployment = {

"cycles": 0,

"Rfree": [np.array([1.03, 1.03, 1.03, 1.03])],

"LivPrb": [np.array([0.98, 0.98, 0.98, 0.98])],

"PermGroFac": [np.array([1.0, 1.0, 1.0, 1.0])],

"UnempDur": 5.0, # Average length of unemployment spell

"BoomDur": 100.0, # Average length of good state

"BustDur": 20.0, # Average length of bad state

"UrateG": 0.05, # Unemployment rate when economy is in good state

"UrateB": 0.12, # Unemployment rate when economy is in bad state

"constructors": {

"MrkvArray": make_serial_unemployment_boombust_mrkv,

"IncShkDstn": None,

"PermShkDstn": None,

"TranShkDstn": None,

},

}

SerialUnemploymentExample = MarkovConsumerType(**init_serial_unemployment)

The SerialUnemploymentExample has no IncShkDstn attribute at this time, so we need to manually specify it now.

[6]:

# Fill in the income distribution with a custom one

employed_income_dist = DiscreteDistributionLabeled(

pmv=np.ones(1),

atoms=np.array([[1.0], [1.0]]),

var_names=["PermShk", "TranShk"],

) # Definitely get income

unemployed_income_dist = DiscreteDistributionLabeled(

pmv=np.ones(1),

atoms=np.array([[1.0], [0.0]]),

var_names=["PermShk", "TranShk"],

) # Definitely don't

SerialUnemploymentExample.IncShkDstn = [

[

employed_income_dist,

unemployed_income_dist,

employed_income_dist,

unemployed_income_dist,

],

]

Now the serial unemployment model is ready to be solved!

[7]:

# Solve the serial unemployment consumer's problem and display solution

t0 = time()

SerialUnemploymentExample.solve()

t1 = time()

print(

"Solving a Markov consumer with serially correlated unemployment took "

+ mystr(t1 - t0)

+ " seconds.",

)

Solving a Markov consumer with serially correlated unemployment took 0.3751 seconds.

[8]:

plt.ylim(0.0, 3.6)

plot_funcs(

SerialUnemploymentExample.solution[0].cFunc,

0.0,

50,

xlabel=r"Market resources $m_t$",

ylabel=r"Consumption $c_t$",

)

In this plot, the blue curve represents the consumption function when employed in good times, and the green curve is the consumption function when employed in bad times. Because the agents are more likely to become unemployed in bad times, they consume a little less as additional buffer.

The orange curve is the consumption function when unemployed in good times, and the red curve is the consumption function in bad times. Unsurprisingly, they are lower than the employed consumption functions, especially at lower levels of \(m_t\) (when the agent is at risk of running out of resources). The “bad times” consumption function is lower than the “good times” one… but not by very much. What’s going on? Shouldn’t someone unemployed in bad times consume very conservatively? In this model, we specified “bad times” as being more likely to become unemployed, but with the same rate of recovering from being unemployed. If you are unemployed during a bust, the bad thing has already happened. Relative to being in good times, the only difference is that once you become re-employed, you are more likely to become unemployed again. That’s a pretty thin margin, thus the small difference in consumption functions.

Unemployment immunity for a fixed period#

Now let’s create the model for a consumer who occasionally gets “unemployment immunity” for a fixed period. That is, every so often the consumer learns that they have been blessed and cannot become unemployed for the next \(N\) periods. When employed, the agent receives constant income; when unemployed, they get no income. We will also remove the artificial borrowing constraint to make the effects of the good news more apparent.

Somewhat unintuitively, this model has \(N+2\) discrete states. The last state index N+1 represents “ordinary times” with binary income and no “unemployment immunity”. State index 0 is someone who has just learned that they have been granted unemployment immunity for \(N\) periods; they were subject to a binary income realization at the start of this period. The intermediate \(N\) periods are when the agent has \(N-1, N-2, \cdots, 0\) periods of unemployment immunity

remaining. The \(0\) periods remaining has its own state because the income distribution in that state is different from ordinary times, and we don’t allow the agent to immediately regain immunity; they must be in normal times for at least one period.

With this setup, we can use another of HARK’s constructors for MrkvArray , called make_ratchet_markov . In a “ratchet Markov” array, transitions only go in one direction, and only one step at a time. The transition from the last state goes back to the first state, or can be set as an absorbing state by specifying its “ratchet probability” as \(0\). This constructor function will be called from within our own custom constructor, defined below.

[9]:

# Define a custom constructor for MrkvArray that uses make_ratchet_markov

def make_unemp_immunity_mrkv(ImmunityPrb, ImmunityT, T_cycle):

"""

Make a list of repeated Markov transition arrays for the "unemployment immunity" model.

Parameters

----------

ImmunityPrb : float

Probability of gaining "unemployment immunity" when in normal times.

ImmunityT : int

Number of periods that unemployment immunity is gained for.

T_cycle : int

Number of periods in this agent's sequence; only used to determine list length.

Returns

-------

MrkvArray : [np.array]

Length T_cycle list of repeated "unemployment immunity" Markov arrays.

"""

ratchet_probs = T_cycle * [

np.concatenate((np.ones(1 + ImmunityT), np.array([ImmunityPrb])))

]

MrkvArray = make_ratchet_markov(T_cycle, ratchet_probs)

return MrkvArray

The income distribution depends on the length of unemployment immunity, so let’s make a constructor for it as well.

[10]:

# Make a custom constructor for IncShkDstn for the unemployment immunity model

def make_unemp_immunity_incshkdstn(UnempPrb, ImmunityT, T_cycle):

"""

Make a list of repeated state-dependent income shock distributions for the "unemployment immunity" model.

Parameters

----------

UnempPrb : float

Probability of getting zero income during normal times.

ImmunityT : int

Number of periods that unemployment immunity is gained for.

T_cycle : int

Number of periods in this agent's sequence; only used to determine list length.

Returns

-------

IncShkDstn : [[DiscreteDistribution]]

Length T_cycle nested list, repeating the same state-dependent income shock distribution.

"""

IncShkDstnReg = DiscreteDistributionLabeled(

pmv=np.array([1 - UnempPrb, UnempPrb]),

atoms=np.array([[1.0, 1.0], [1.0, 0.0]]),

var_names=["PermShk", "TranShk"],

) # Ordinary income distribution

IncShkDstnImm = DiscreteDistributionLabeled(

pmv=np.array([1.0]),

atoms=np.array([[1.0], [1.0]]),

var_names=["PermShk", "TranShk"],

) # Immune income distribution

IncShkDstn_t = [IncShkDstnReg] + ImmunityT * [IncShkDstnImm] + [IncShkDstnReg]

IncShkDstn = T_cycle * [IncShkDstn_t]

return IncShkDstn

Now we can make and solve an instance of MrkvConsumerType to represent this model.

[11]:

# Make a consumer who occasionally gets "unemployment immunity" for a fixed period

ImmunityT = 6 # Number of periods of immunity

N = ImmunityT + 2

init_unemployment_immunity = {

"UnempPrb": 0.05, # Probability of becoming unemployed each period

"ImmunityPrb": 0.01, # Probability of becoming "immune" to unemployment

"ImmunityT": 6, # Number of periods of immunity

"Rfree": [1.02 * np.ones(N)],

"LivPrb": [0.98 * np.ones(N)],

"PermGroFac": [1.01 * np.ones(N)],

"BoroCnstArt": None,

"CubicBool": True,

"cycles": 0,

"constructors": {

"MrkvArray": make_unemp_immunity_mrkv,

"IncShkDstn": make_unemp_immunity_incshkdstn,

},

}

ImmunityExample = MarkovConsumerType(**init_unemployment_immunity)

[12]:

# Solve the unemployment immunity problem and display the consumption functions

t0 = time()

ImmunityExample.solve()

t1 = time()

print(

'Solving an "unemployment immunity" consumer took ' + mystr(t1 - t0) + " seconds.",

)

Solving an "unemployment immunity" consumer took 0.6922 seconds.

[13]:

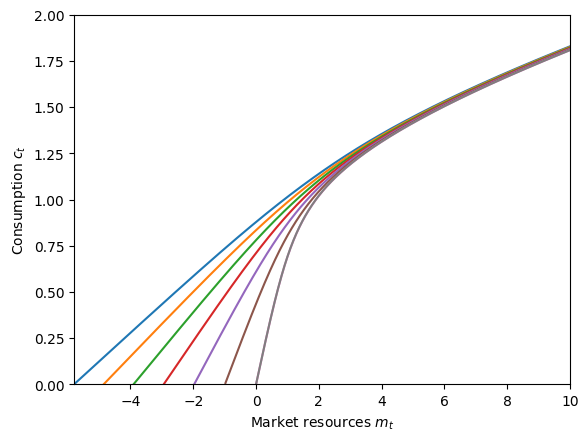

mNrmMin = np.min([ImmunityExample.solution[0].mNrmMin[j] for j in range(N)])

plt.ylim(0.0, 2.0)

plot_funcs(

ImmunityExample.solution[0].cFunc,

mNrmMin,

10.0,

xlabel=r"Market resources $m_t$",

ylabel=r"Consumption $c_t$",

)

C:\Users\Matthew\Documents\GitHub\HARK\HARK\interpolation.py:2248: RuntimeWarning: All-NaN slice encountered

y = self.compare(fx, axis=1)

The blue consumption function represents when the consumer has just learned that they are guaranteed to receive income for the next \(N\) periods. Because there is no artificial borrowing constraint, they can borrow against future earnings. Thus the consumption functions for agents with temporary unemployment immunity are defined below zero. Agents in normal times and those who are in their final immunity period have almost identical consumption functions, but “normal times” are slightly better: the agent has some hope that they will be granted immunity next period, but the agent in their last period must go to normal times for at least one period. We can plot the difference between these consumption functions to verify.

[14]:

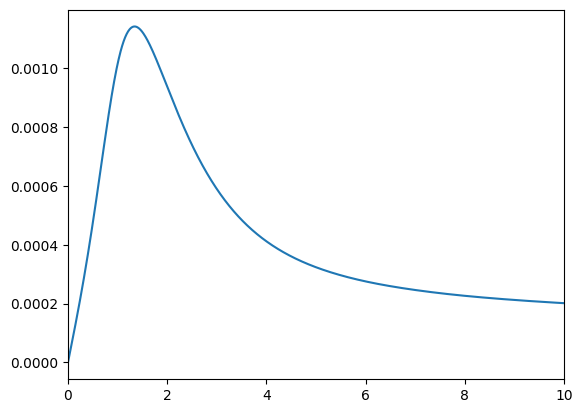

# Plot the difference between consumption functions in normal times and when immunity has just expired

f = lambda m: ImmunityExample.solution[0].cFunc[-1](m) - ImmunityExample.solution[

0

].cFunc[-2](m)

plot_funcs(f, 0.0, 10.0)

Yep: the agent consumes just barely more in normal times!

Serial permanent income growth#

Finally, we’ll make a MarkovConsumerType with serially correlated income growth. We’ll use the standard income shock process within each state, but have different average permanent income growth within each state, through PermGroFac . The Markov transition process will specify the persistence of all state, with a random state selected with complementary probability (including remaining in the same state).

First, let’s define our custom “persistence Markov” process.

[15]:

# Define a constructor for the "random persistence" process

def make_random_persistence_mrkv(StateCount, Persistence, T_cycle):

"""

Make a repeated list of Markov transition arrays with specified state persistence on the diagonal and uniform transitions off it.

Parameters

----------

StateCount : int

The number of discrete states.

Persistence : float

The probability of (being guaranteed to) remain in the current state.

T_cycle : int

The number of periods in this agent's sequence, used only for the length of the list.

Returns

-------

MrkvArray : [np.array]

Length T_cycle repeated list of persistence Markov transition arrays.

"""

on_diag = Persistence * np.eye(StateCount)

off_diag = (1.0 - Persistence) / StateCount * np.ones((StateCount, StateCount))

MrkvArray_t = on_diag + off_diag

MrkvArray = T_cycle * [MrkvArray_t]

return MrkvArray

Now we can make a parameter dictionary. When using the default income shock process constructors, we specify PermShkStd and TranShkStd (etc) as arrays of shape (T_cycle, StateCount) with the same value in all entries. We’ll set the persistence factor fairly high (80%) and have a wide spread of permanent income growth rates.

[16]:

# Make a consumer with serially correlated permanent income growth

N = 5 # Number of permanent income growth rates

PermGroFacMin = 0.97

PermGroFacMax = 1.05

init_serial_growth = {

"LivPrb": [0.98 * np.ones(N)],

"PermGroFac": [np.linspace(PermGroFacMin, PermGroFacMax, N)],

"Rfree": [1.02 * np.ones(N)],

"PermShkStd": 0.1 * np.ones((1, N)),

"TranShkStd": 0.1 * np.ones((1, N)),

"IncUnemp": np.zeros((1, N)),

"UnempPrb": 0.05 * np.ones((1, N)),

"Persistence": 0.8,

"StateCount": N,

"cycles": 0,

"constructors": {"MrkvArray": make_random_persistence_mrkv},

}

SerialGroExample = MarkovConsumerType(**init_serial_growth)

[17]:

# Solve the serially correlated permanent growth shock problem and display the consumption functions

t0 = time()

SerialGroExample.solve()

t1 = time()

print(

"Solving a serially correlated growth consumer took "

+ mystr(t1 - t0)

+ " seconds.",

)

plt.xlabel(r"Market resources $m_t$")

plt.ylabel(r"Consumption $c_t$")

plt.ylim(0.0, 2.0)

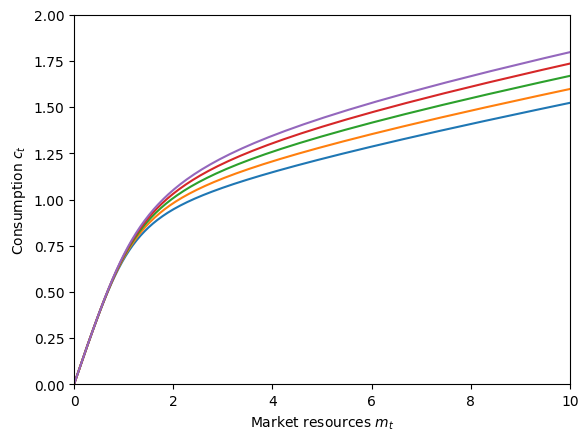

plot_funcs(SerialGroExample.solution[0].cFunc, 0, 10)

Solving a serially correlated growth consumer took 1.3412 seconds.

The consumption functions are ordered from lowest permanent income growth (blue) to highest (purple). As we would expect, the agent wants to consume more now when they expect their income to rise rapidly in the future, and to consume less when they expect their income to fall for a while.

You can use these examples to try constructing your own unusual models; MarkovConsumerType is pretty flexible!